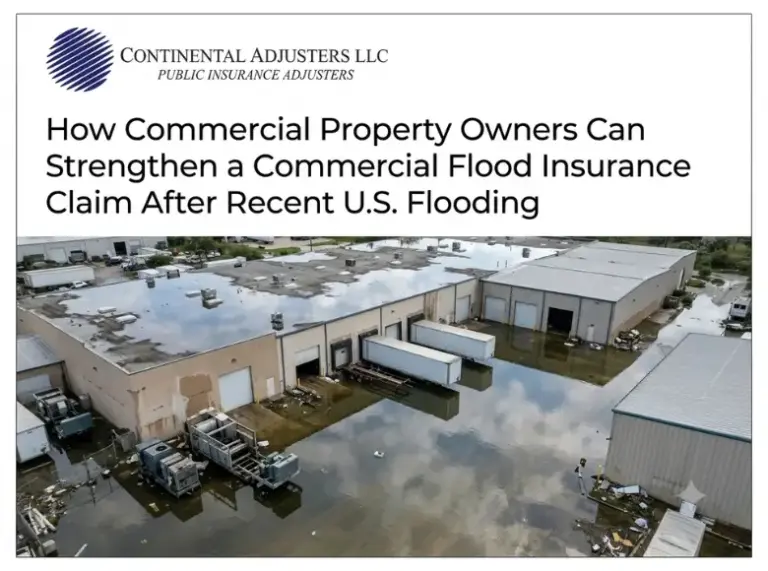

Floodwater doesn’t take your insurance policy into account before it enters your building. One day your business is open and running like any other. The next day, a storm rolls through, water rises fast, and you are left with ruined inventory, damaged property, and a growing list of questions your insurer expects you to have the answers to.

Commercial property owners were faced with this situation after severe flooding hit parts of New York City and Long Island in May 2026. Business owners in other flood-prone regions face the same challenge every storm season.

This guide walks through how to build a stronger commercial flood insurance claim, avoid the mistakes that slow down settlements, and quickly get your business back to full operation.

Why Commercial Flood Claims Get Complicated Fast

Flood claims involve more moving parts than most other property losses. Separate policies, strict filing rules, and disputes over the cause of damage all can slow the process down.

Flood insurance pays far more than federal disaster aid. Between 2016 and 2022, the National Flood Insurance Program paid an average claim of more than $66,000. FEMA disaster assistance grants averaged just $3,000 over that same period, according to FEMA’s flood insurance fact sheet.

Common reasons commercial flood claims stall:

- Confusion between NFIP flood coverage and standard commercial property policies

- Disputes over whether damage came from flooding or another covered peril

- Missing pre-loss records showing the building’s prior condition

- Business interruption losses that were never properly calculated

- Delayed reporting that gives insurers room to question the timeline

Recent Flooding Shows Why Preparation Matters

Severe storms struck the New York City area on May 20, 2026, causing significant flooding across Queens and the surrounding boroughs. Governor Kathy Hochul secured a physical disaster declaration from the U.S. Small Business Administration for businesses that were impacted by severe flooding in Queens, Bronx, Kings, Nassau, New York, and Richmond counties, according to an official announcement from the Governor’s office. A joint damage assessment by state officials confirmed major damage to multiple commercial properties in the affected area. This event follows a pattern seen across the country in recent years, where commercial buildings once considered low risk take on significant water damage during short, intense storms.

This gap between what a storm destroys and what gets paid out through insurance repeats after nearly every major flood event. Federal disaster assistance rarely covers the full cost of restoring a commercial property, based on guidance published on FEMA’s disaster assistance page. That gap is exactly why a well-documented commercial flood insurance claim matters so much.

Steps to Strengthen Your Commercial Flood Insurance Claim

1. Report the Loss Right Away

Contact your insurer and file your claim as soon as it is safe to enter the property. Delayed reporting can raise questions about the cause and timing of damage.

2. Document Everything Before Cleanup Begins

Photograph and record video of every affected area before repairs start. Include:

- Water lines on walls and equipment

- Damaged inventory, fixtures, and machinery

- Structural damage to floors, walls, and foundations

- Debris and contamination brought in by floodwater

3. Separate Structural Damage From Business Interruption Losses

Commercial flood claims often focus only on physical damage. Lost income, extra operating expenses, and payroll costs during a closure deserve their own documented claim.

| Loss Category | Examples | Documentation Needed |

| Structural Damage | Walls, flooring, foundation, HVAC | Photos, contractor estimates, inspection reports |

| Contents and Inventory | Equipment, stock, fixtures | Purchase receipts, replacement cost estimates |

| Business Interruption | Lost revenue, closed operations | Financial statements, tax returns, sales history |

| Extra Expense | Temporary space, equipment rental | Invoices, lease agreements, receipts |

4. Get an Independent Damage Assessment

Insurance company adjusters work for the carrier. An independent evaluation gives your business a second, unbiased assessment of the full scope of damage before you accept a settlement offer.

5. Track Every Recovery Cost

Save receipts for water extraction, drying equipment, temporary repairs, and any steps taken to prevent further damage. Insurers often reimburse reasonable mitigation costs.

6. Review Your Policy Language Closely

Commercial property policies and NFIP flood policies define “flood” differently than most business owners expect. Confirm what triggers coverage, what exclusions apply, and how your deductible works before you negotiate a settlement.

How Continental Adjusters Can Help

Rebuilding a commercial flood insurance claim on your own puts your business at a disadvantage against a carrier’s adjusting team. Continental Adjusters represents policyholders only, never insurance carriers, and brings the right expertise to each stage of the recovery process.

- Public Adjuster services: Our team inspects the property, documents the full scope of damage, and manages the claim negotiation so your business does not have to face the carrier alone.

- Forensic Accounting: When business interruption losses need to be calculated accurately, our forensic accountants build a defensible financial picture of lost revenue and extra expense.

- Expert Witness support: For claims headed toward litigation or arbitration, our team provides testimony grounded in commercial property and claims expertise.

- Umpire and Appraisals: When a carrier’s valuation falls short, our appraisal and umpire services help resolve disputes over the true value of a commercial property loss.

Case Study: Water Damage Claim Settlement Increase

A country club property suffered significant water damage after a flood event affected the building. The insurer’s initial estimate for repairs came in at $1.1 million.

The property owner brought in Continental Adjusters to lead the claim. Using industry expertise, deep policy knowledge, and a multi-approach negotiation strategy, the team built a stronger, better-documented case for the full scope of the loss.

The claim ultimately settled for $4.3 million, nearly four times the insurer’s original offer. These documentation and negotiation principles apply directly to all commercial flood claims: a thorough, well-supported case gives an insurer far less room to undervalue the loss.

Common Mistakes That Weaken Commercial Flood Claims

- Accepting the first settlement offer without an independent review

- Discarding damaged inventory or materials before documenting them

- Failing to track business interruption losses from day one

- Assuming a commercial property policy automatically includes flood coverage

- Missing NFIP filing deadlines

Frequently Asked Questions

Does a standard commercial property policy cover flood damage?

Most standard commercial property policies exclude flood damage caused by rising water, storm surge, or surface flooding. Separate flood coverage through the NFIP or a private flood policy is usually required.

How long do I have to file a commercial flood insurance claim?

Deadlines vary by policy and by disaster declaration. NFIP policies typically require proof of loss within 60 days, though extensions are sometimes granted after major disasters. Check your policy and any FEMA disaster announcements for updated deadlines.

Can I claim lost business income after a flood?

Yes, if your policy includes business interruption or extra expense coverage. You will need financial records showing income before and after the flood to support the claim.

What if my insurer undervalues my flood damage?

You can request a second inspection, hire an independent public adjuster, or invoke your policy’s appraisal clause if you believe the settlement offer is too low.

Should I start repairs before the adjuster visits?

Only make repairs necessary to prevent further damage. Document the property thoroughly with photos and video before any cleanup or reconstruction begins.

Does FEMA or SBA assistance replace insurance coverage?

No. Federal aid is meant to supplement, not replace, insurance. Federal assistance caps are often far lower than the actual cost of restoring a commercial property.

Final Thoughts

Flood damage puts pressure on every part of a business, from the building itself to the income it generates. A commercial flood insurance claim built on strong documentation, accurate valuation, and a clear understanding of your policy gives your business the best chance at full recovery.

If your commercial property was affected by recent flooding and you are unsure whether your settlement offer reflects the true cost of your loss, Continental Adjusters can review your claim and help you build the case your business deserves. Contact our team to discuss your commercial flood insurance claim.